Executive Summary

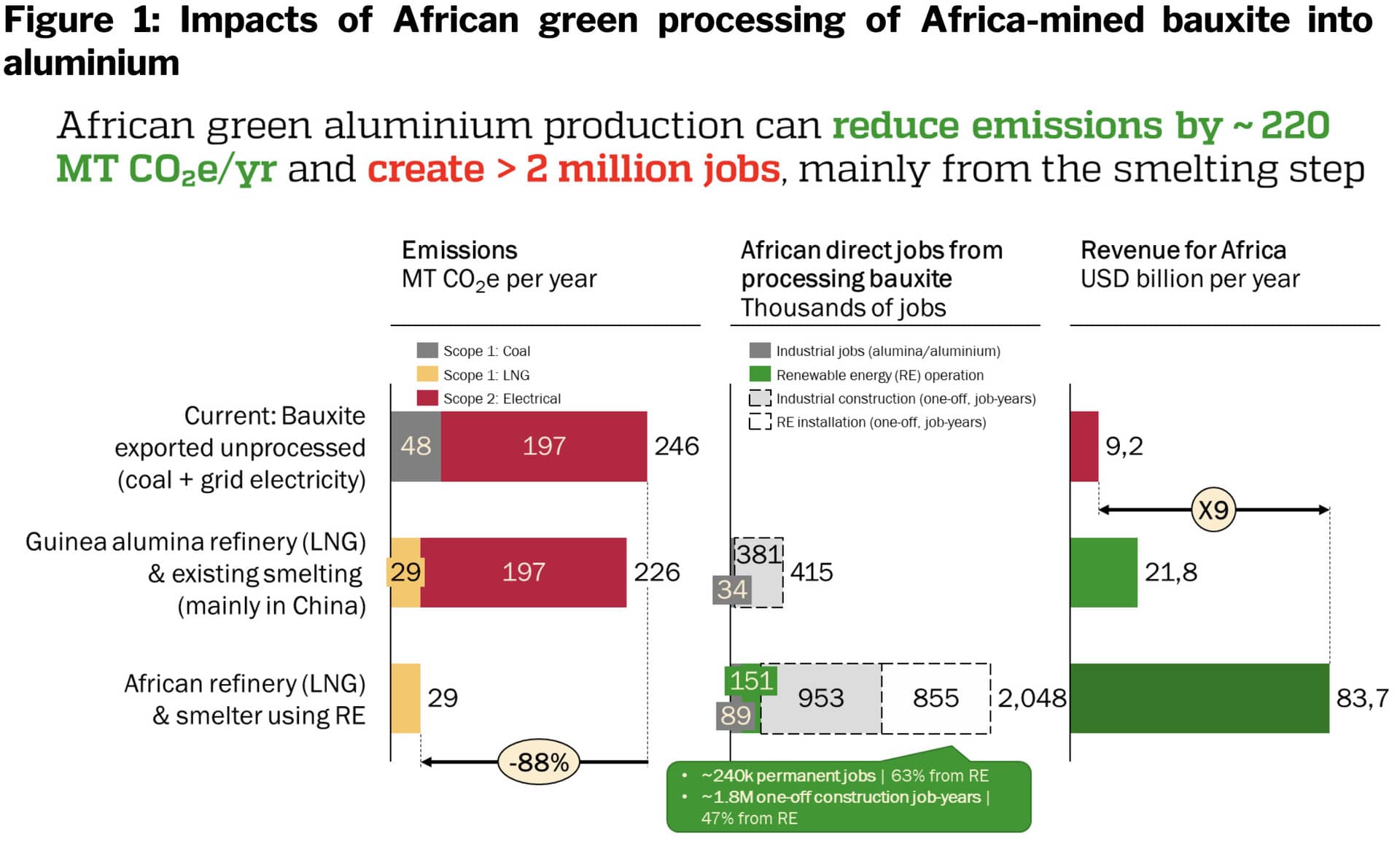

Locally processing all Africa-mined bauxite into aluminium using renewable energy could generate 240,000 permanent jobs and 1.8 million one-off construction job-years — alongside 220 MT CO₂e in annual emissions reductions and nearly $84 billion in export revenue.

Africa currently exports almost all the bauxite it mines. The refining and smelting steps — where revenue multiplies and emissions are generated — happen elsewhere, powered largely by fossil energy. That is a structural misallocation of both economic and climate resources.

And while mineral processing features increasingly in African industrialisation discussions, this is the first time the employment, climate, and revenue potential of green aluminium production in Africa has been fully scoped. The methodology developed here builds on and replicates the approach applied to green iron (HBI) production, providing a consistent, evidence-based framework for assessing Africa’s green industrial opportunities across energy-intensive value chains.

Download PDF Version

Representing nearly a quarter of the global bauxite production, this opportunity is one of the largest possible global shifts towards industrial decarbonisation. Requiring baseload power at an unprecedented scale, it would underpin an entirely new energy system. A system that combines different types of RE, both baseload such as geothermal and hydro, and intermittent solar and wind for which Africa has uniquely high capacity factors and limited competing use, alongside large-scale short-term storage. This must include effective distribution and transmission and power pools to support grid management and load balancing for continental collaboration. It will require innovations in investment approaches, a shift in trade relationships, and a fundamental valuation of the low embedded carbon.

Globally, aluminium smelting consumes enormous volumes of electricity for a proportionally small share of economic output. Matching that demand to the world’s largest untapped renewable energy resource is both a global efficiency gain and offers long-term pathways to resilience and independence of fuel supply chain disruptions. It is an unprecedented transformation that will be a cornerstone of African green industrialisation, industrial decarbonisation and globally efficient renewable energy use and is necessary to stay on track towards global net zero by 2050. We have no time to lose.

1. Africa’s Industrial Opportunity: Processing Bauxite at the Source

Africa has the raw material, untapped Renewable Energy (RE) potential, and the workforce to become a global producer of green aluminium. Guinea realises 95–98% of African bauxite exports. Virtually all Africa-mined bauxite is exported unprocessed, primarily to China, where it is refined into alumina and smelted into aluminium using fossil-intensive energy systems.

This pattern replicates across extractive industries continent-wide: Africa exports the raw commodity and forfeits the industrial value. In aluminium, the value multiplication is stark. Africa’s bauxite exports generate approximately $9.2 billion per year. Retaining the refining and smelting steps on the continent would increase that figure to nearly $83.7 billion — a ninefold increase.

New jobs, new value, new capability

Processing all bauxite exported from Africa into green aluminium would:

- Generate ~240,000 permanent operational jobs, with 63% driven by RE operation, and ~1.8 million construction job-years, split roughly equally between industrial facility build-out and the renewable energy infrastructure that powers it.

- Reduce associated emissions from 246 MT to 29 MT CO₂e, avoiding ~220 MT each year — an 88% reduction.

- Retain nearly $84 billion annually on the continent, up from $9.2 billion in raw bauxite exports.

The majority of jobs stem from Africa’s renewable-energy build-out and operation, underscoring the centrality of clean energy in enabling competitive green industry. The smelting step — the most electricity-intensive stage of aluminium production — drives the bulk of both the employment and the emissions reduction potential.

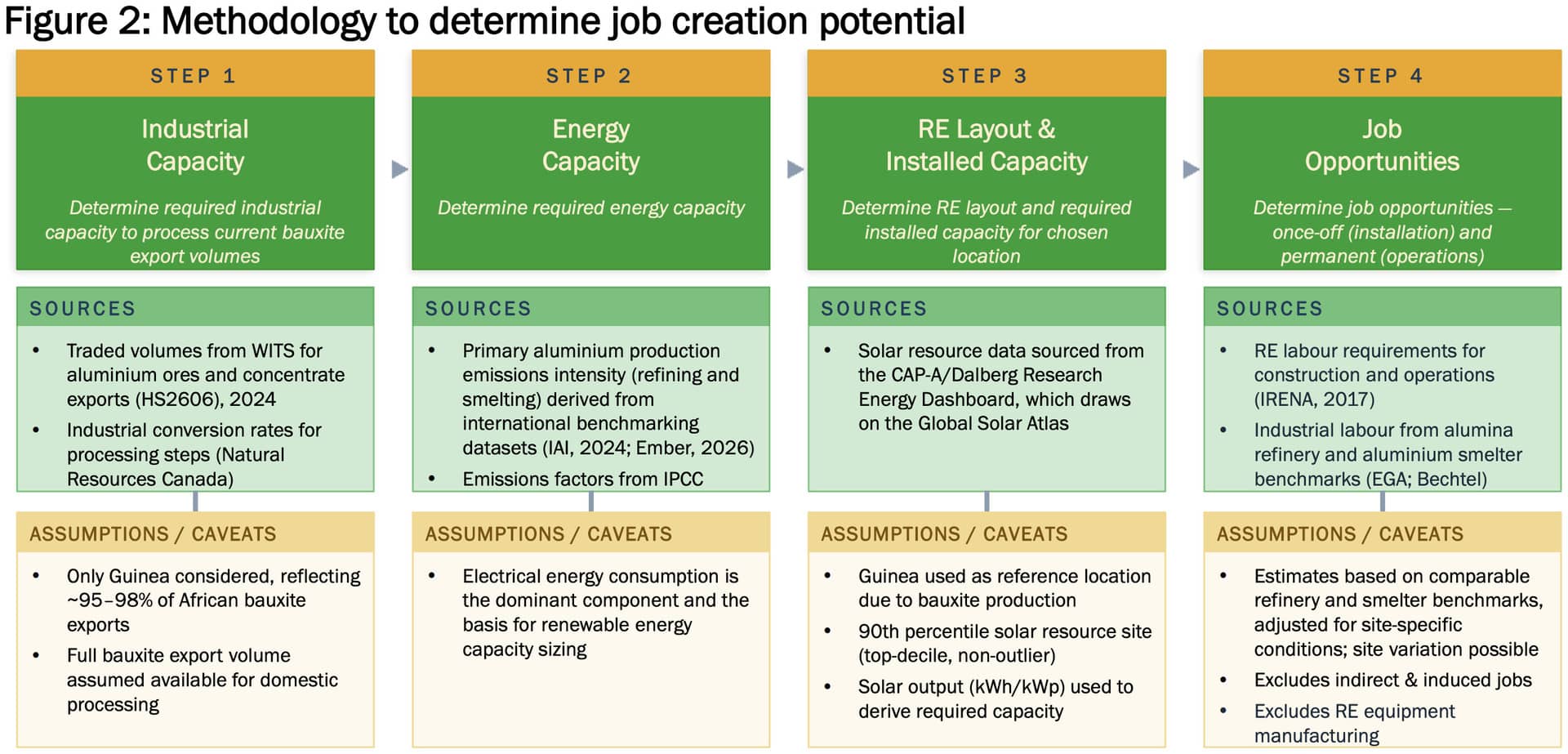

Methodology: Estimating job opportunities

Figure 2 details the methodology and assumptions. A bibliography of sources can be found in the Annex. Jobs associated with load balancing and storage in the broader energy system transformation are not included.

2. Global Climate Impact: ~220 MT CO₂e of Emissions Reduced

Shifting aluminium processing to Africa and powering it with renewable energy would cut global emissions associated with African bauxite from 246 MT to 29 MT CO₂e — a ~220 MT annual reduction. This represents an 88% decrease and constitutes one of the single largest decarbonisation levers available in the global aluminium system.

The emissions profile of aluminium production is dominated by electricity consumption in the smelting step. Notwithstanding a global shift towards increased use of renewable energy, many current smelting destinations — primarily China — still have a substantial portion of coal-based grid electricity, which accounts for the majority of associated emissions (Scope 2). Processing in Africa using renewable energy for smelting eliminates these electrical emissions entirely. Thermal emissions from the refining step are reduced but not eliminated, with LNG replacing coal as the near-term transition fuel (Scope 1).

The refining step alone — producing alumina in Guinea using LNG, without relocating smelting — would reduce emissions from 246 MT to 226 MT CO₂e. The transformational reduction comes from the smelting step: combining African refining with renewable-powered smelting drives the full reduction to 29 MT CO₂e. This underscores that smelting is where the climate leverage sits.

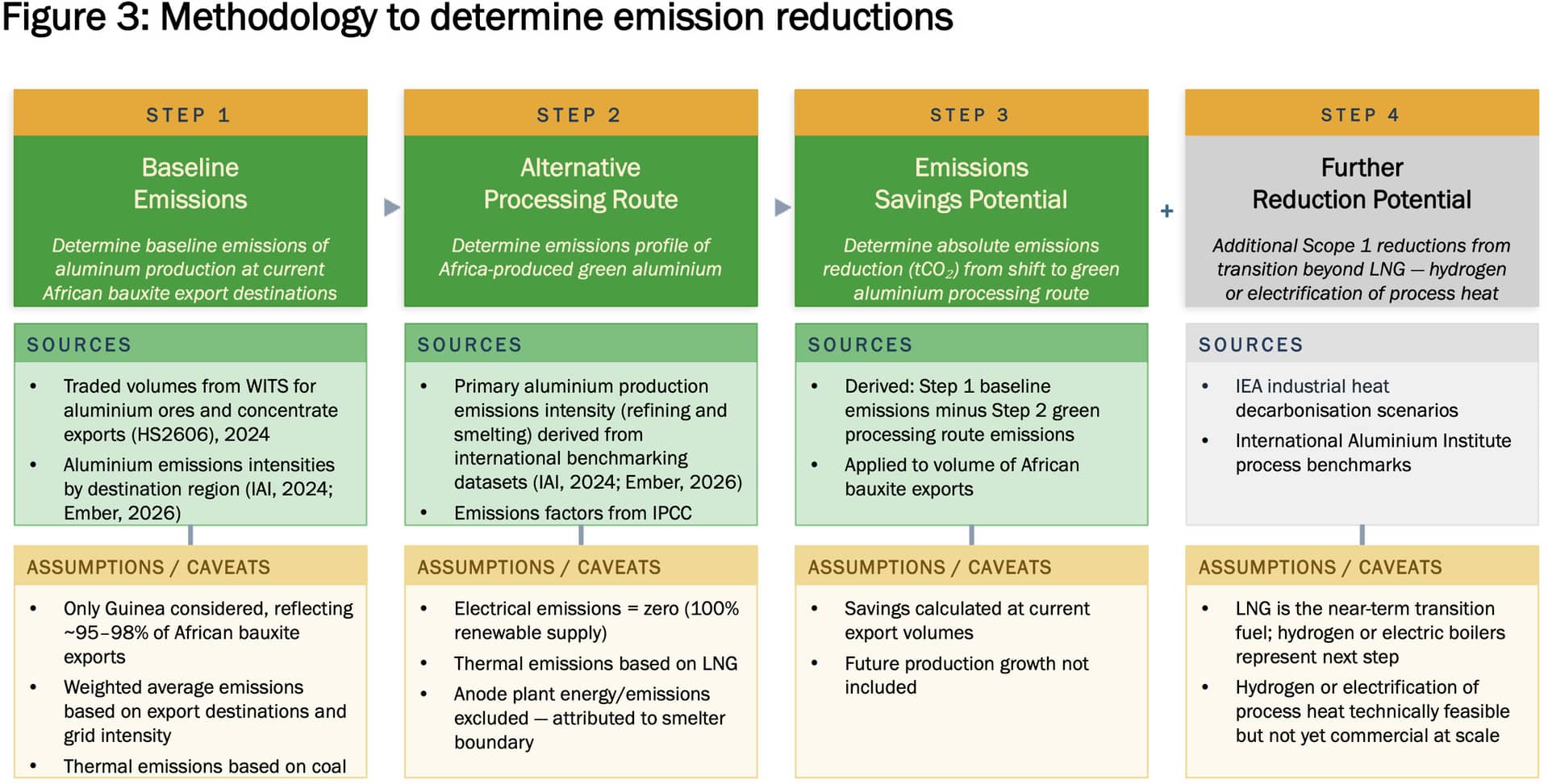

Methodology: Estimating emissions reductions

Baseline emissions were calculated by assessing current destination-country emissions processing African bauxite exports. In this analysis, we opted to use average national grid intensity. Even with captive power, using average national grid intensity is appropriate given the fungible nature of electricity paired with a global tendency of growing generation capacity and an ambition to decarbonise grids. In other words: the ‘climate opportunity cost’ of the aluminium industry comes from the fact that (captive) power used for smelters cannot be used elsewhere. Renewable captive power is not available to decarbonising a (growing) grid or, as is the case in China, smelters use many coal-based captive power plants. Figure 3 includes further detail and assumptions, with sources detailed in the Annex.

3. The Window of Opportunity: Why Timing Matters

Unlike green iron, where Africa’s processing advantage aligns with strategic imperatives from off-takers, aluminium presents a more contested landscape. Incumbent regions, particularly China, are aware of the emissions penalty of fossil-powered smelting, and associated risks to competitiveness once emissions are fully priced in. They are acting accordingly.

Aluminium smelting drives ~5% of China’s emissions, and consumes ~ 5 – 7% of its total electricity consumption, whilst generating well below 1% of GDP. This energy inefficiency is at the root of various shifts and decisions:

- Consistent policy context around aluminium in particular: Since 2017, the Chinese government has enforced a cap of 45 million tonnes per year on primary aluminium capacity to address overcapacity issues, manage energy security concerns, and reduce carbon emissions. The 15th Five-Year Plan (2026 – 2030) extends this policy with a continued focus on “dual control,” which limits both production capacity and energy consumption

- Industrial renewable energy targets: the National Development and Reform Commission issued mandatory renewable electricity consumption targets, with aluminium being the first industry this was applied to. The target varies by province and ranges from 25% to 70%

- As a result, the industry structure is shifting:

- On one hand, Chinese smelting capacity is internally relocated to provinces with greater hydroelectric and renewable resources.

- On the other hand, China is investing at substantial scale in aluminium refineries and smelters in Indonesia. This responds to Indonesia’s bauxite export ban, secures continued access to Indonesian bauxite, and helps grow aluminium production whilst staying within China’s domestic capacity cap.

This shows strategic alignment and an explicit willingness to invest internationally in this sector. Yet it also creates urgency. If China rebuilds its smelting capacity near domestic RE resources in a way that appropriately addresses the opportunity costs, the structural case for shifting production to Africa weakens. The energy arbitrage that gives Africa its competitive edge exists precisely because incumbent smelters are currently locked into fossil-intensive systems and face high opportunity costs for their RE. That is not here to stay.

The global efficiency argument is straightforward: aluminium smelting consumes enormous volumes of electricity for a proportionally small share of economic output. Allowing the most energy-intensive processing step to migrate to the locations with the greatest renewable energy surplus — Africa prominent among them — frees constrained electricity systems elsewhere for higher-value uses. Africa’s solar, wind, and geothermal endowment is among the strongest in the world, providing the basis to become globally cost-competitive in renewable generation and thus in renewable-powered smelting.

This logic holds if the shift happens before incumbents rebuild domestically. New industrial and trade relationships are needed to create mutual benefits, with continued access to aluminium and the ability for all actors to deploy their energy potential to the economic activities with the greatest value add. The window is measured in years, not decades.

Sourced from FastMarkets: https://www.fastmarkets.com/insights/base-metals-demand-outlookunder-chinas-15th-five-year-plan-reactive-analysis/

4. Capturing the Opportunity: What Needs to Be in Place

Green aluminium is not a climate project with development co-benefits. It is an industrial development strategy with a superior emissions profile: one that generates the fiscal revenues, employment, and manufacturing capacity that make climate commitments politically sustainable for African governments.

The advantage either gets captured through deliberate action or defaults to incumbents. African governments can offer investors something fossil-dependent regions cannot: a clean-slate energy system designed around industrial load from the outset, paired with bauxite reserves and renewable energy resources capable of sustained round-the-clock smelting. Capturing the opportunity requires action across four dimensions.

Fundamental energy system transformation

Representing nearly a quarter of the global bauxite production, this opportunity is one of the largest possible global shifts towards industrial decarbonisation. Even a gradual build-up requires a fundamental energy system rethink. Requiring continuous baseload, this type and scale of industrial processing would underpin an energy system that brings together different types of renewable energy, both baseload such as geothermal and hydro, and intermittent solar and wind for which Africa has uniquely high capacity factors and limited competing use, coupled with large-scale short-term storage. Effective distribution and transmission, including large power pools will be necessary for grid management and load balancing for continental collaboration. These are the characteristics of the energy system the world needs for long-term sustainability. Africa’s very small existing industrial and energy footprint allows the continent to build this out future-proof from the start.

Structured off-take agreements

Capital-intensive smelter and refinery projects require long-term revenue certainty. Structured offtake agreements with industrial buyers and traders provide the demand-side anchor that makes projects financeable. Without committed buyers, the cost of capital remains prohibitively high regardless of Africa’s renewable energy advantage.

Regulatory recognition of embedded emissions

Frameworks such as the EU Carbon Border Adjustment Mechanism (CBAM) must recognise the emissions profile of smelting electricity, ensuring that green aluminium produced with African renewable energy receives the price signal advantage it warrants over fossil-produced aluminium. The EU CBAM currently does not include these scope 2 emissions for aluminium. If rules for pricing embedded carbon, currently expanding globally, do not adequately differentiate between production powered by African renewables and production powered by fossil fuels, the market signal that would drive the shift is suppressed, hampering global industrial decarbonisation.

Investment structuring that lowers the cost of capital

Africa’s renewable energy is abundant, but it is not yet cheap — the cost of capital, not the cost of generation, is the binding constraint. De-risking instruments, blended finance structures, project finance, and development finance interventions are needed to bring the financing cost of African renewable-powered industry into a range that reflects the underlying resource quality rather than the (perceived) sovereign risk.

5. Evolving and Expanding This Methodology

Caveats to this methodology and priorities for its evolution

This methodology allows users to understand potential impacts of green industrialisation in a specific sector, simultaneously assessing job creation, economic value and emission outcomes. To achieve methodological consistency and comparability of results in a space of limited jobs data, the jobs estimates are anchored on assuming a location-specific optimal mix of solar and wind energy – both intermittent sources. This is a deliberate simplification that assumes opportunities are embedded in broader, load balanced power systems providing necessary baseload capacity; and any further consideration of specific opportunities most take power needs into account in detail, and embed them into system design. That needs to happen everywhere in the world – and is increasingly a question we cannot resolve solely with baseload sources as the need for and pace of electrification exceeds the ability to make renewable baseload available. Rapid advances and cost reductions in (short-term) storage will be key to achieving this global transformation. As we evolve the methodology, we look to update and refine reliable and comparable job multipliers, that also allow to model more sophisticated energy system setups.

This methodology does not assess or confirm location-specific or economic viability. At a macro-economic level, it must be complemented by an opportunity-specific analysis of competitive and comparative advantage. When translating the sectoral potential into specific opportunities, further work is needed to shape win-win opportunities for investments, develop and deploy focused interventions to reduce the cost of capital, and assess location-specific suitability, confirming key requirements are or can be put in place.

Expanding This Methodology

The methodological approach developed for green iron (HBI) and now applied to aluminium provides a replicable framework to assess the potential impact of green industrial development for Africa across energy-intensive value chains. It is designed for any process where competitiveness is fundamentally shaped by access to abundant, reliable, and low-cost renewable energy — including solar, wind, geothermal, and hybrid configurations. These are the processes where Africa’s energy endowment, land availability, and industrial expansion potential combine to offer a distinct strategic edge.

By quantifying baseline production routes, modelling renewable-anchored alternatives, and estimating job creation, economic value, and emissions outcomes, this methodology enables evidence-based prioritisation of Africa’s green industrial opportunities. Job creation is central: high-energy processes require large construction and operational workforces when combined with renewable-energy deployment. Economic value — through retained earnings and upgraded exports — provides a complementary and distinct benefit.

We are currently working on applying this methodology to data centres. Further applications may include green fertilisers, cement substitutes, battery precursor materials, and green chemicals. Used consistently, this methodology becomes a strategic tool for governments, financiers, and investors to determine where Africa can prioritise green industrial development based on the climate, revenue, and job creation benefits each option can realise.

Annex: References and Sources

The following references constitute all sources cited in the two methodology slides (Figures 2 and 3) that underpin the analytical approach used in this report. Please note that labour intensity is an area of much uncertainty. We explored many sources across reported projects, surveys, and academic (including partially modelled) sources. Upon request, we can provide further detail on sources considered and rationale for using the IRENA/ ILO source. As data and insights evolve further, we will adjust the inputs accordingly.

Bechtel, n.d. Ras Al Khair Aluminum Smelter; Al Taweelah Alumina Refinery. Available at: https://www.bechtel.com/projects/ras-al-khair-aluminum-smelter/ ; https://www.bechtel.com/projects/al-taweelah-alumina-refinery/ (Accessed: March 2026).

Climate Action Platform Africa (CAP-A) and Dalberg Research, n.d. Energy Dashboard: Solar and Wind. Available at: https://gisresearch.dalbergresearch.com/cap-a_energydashboard/ (Accessed: February 2026). Dashboard draws on data from the Global Solar Atlas and Global Wind Atlas.

Construction Week, 2024. ‘EGA to build first US aluminium smelter in over 40 years with $4bn investment.’ Available at: https://www.constructionweekonline.com/news/ega-to-build-first-us-aluminium-smelter-in-over-40-years-with-4bn-investment (Accessed: February 2026).

Ember, 2026. Yearly electricity data. Available at: https://ember-energy.org/data/yearly-electricity-data/ (Accessed: February 2026).

Emirates Global Aluminium (EGA), n.d. ‘Al Taweelah alumina refinery.’ Available at: https://www.ega.ae/en/about-us/operations/al-taweelah-alumina-refinery (Accessed: February 2026).

International Aluminium Institute (IAI), 2024. Primary aluminium smelting energy intensity. Available at: https://international-aluminium.org/statistics/primary-aluminium-smelting-energy-intensity/ (Accessed: February 2026).

International Renewable Energy Agency (IRENA), 2017. Renewable energy benefits: Leveraging local capacity for solar PV. Abu Dhabi: IRENA. Available at: https://www.irena.org/-/media/Files/IRENA/Agency/Publication/2017/Jun/IRENA_Leveraging_for_Solar_PV_2017.pdf (Accessed: February 2026).

Natural Resources Canada, n.d. ‘Aluminum facts.’ Available at: https://natural-resources.canada.ca/minerals-mining/mining-data-statistics-analysis/minerals-metals-facts/aluminum-facts (Accessed: February 2026).

World Bank, 2024. World Integrated Trade Solution (WITS): UN Comtrade trade data. Trade statistics for aluminium ores and concentrates (HS 2606). Available at: https://wits.worldbank.org/trade/comtrade/ (Accessed: February 2026).

IPCC, 2006. 2006 IPCC Guidelines for National Greenhouse Gas Inventories. Volume 2: Energy, Chapter 1: Introduction. Hayama: Institute for Global Environmental Strategies (IGES). Available at: https://www.ipcc-nggip.iges.or.jp/public/2006gl/pdf/2_Volume2/V2_1_Ch1_Introduction.pdf (Accessed: March 2026).

About CAP-A

Climate Action Platform – Africa (CAP-A) exists to demonstrate how Africa can achieve inclusive economic growth through climate-action – a focus we call Climate Positive Growth. CAP-A’s work starts from a simple premise: Africa’s structural advantages in untapped renewable energy potential, young and entrepreneurial workforce, and relevant natural assets and resources make it one of the most competitive regions globally for climate action across green industrialisation and manufacturing, climate-smart agriculture, nature protection and carbon removal.

Africa’s unparallelled untapped solar, wind, geothermal and land availability, paired with the continent’s rapidly growing workforce and abundant mineral endowment, and relatively limited existing industrial infrastructure that needs to be dismantled or transitioned away from, positions Africa to lead in the next wave of global green industry.

CAP-A translates this potential into action by generating rigorous, sector- and country-specific evidence on where Africa can compete in low-carbon production. This includes quantifying job creation, assessing renewable-energy requirements, mapping global supply-chain dynamics and identifying opportunities where African production can deliver lower emissions and lower costs than incumbent systems. The green HBI opportunity presented in this report is one such case: a combination of potential for industrial competitiveness, system-level decarbonisation, and large-scale employment anchored in renewable-energy deployment.

Beyond analytics, CAP-A works directly with governments, investors, industrial actors and global rule-shapers to align policy, financing and market access with Africa’s emerging industrial advantage. This includes supporting the conceptualisation of bankable industrial projects, informing trade and industrial policy, showcasing proof-of-concept demonstrations and ensuring African priorities are reflected in global market frameworks. Across all of its work, CAP-A connects economic development and climate ambition, showing that climate-aligned industrialisation is not a trade-off but a pathway to long-term competitiveness, job growth, and inclusive development.

CAP-A Co-Founder Carlijn Nouwen is the lead author for this report. CAP-A staff member Matthew Hill provided much of the analytical work shaping the findings of the quantification. Dr Jasper Grosskurth and his team at LOCAN/ DR helped establish the location-specific multipliers to determine required installed capacity.

Please contact us at info@cap-a.org if you have any questions, comments, or suggestions. We look forward to hearing from and partnering with you.